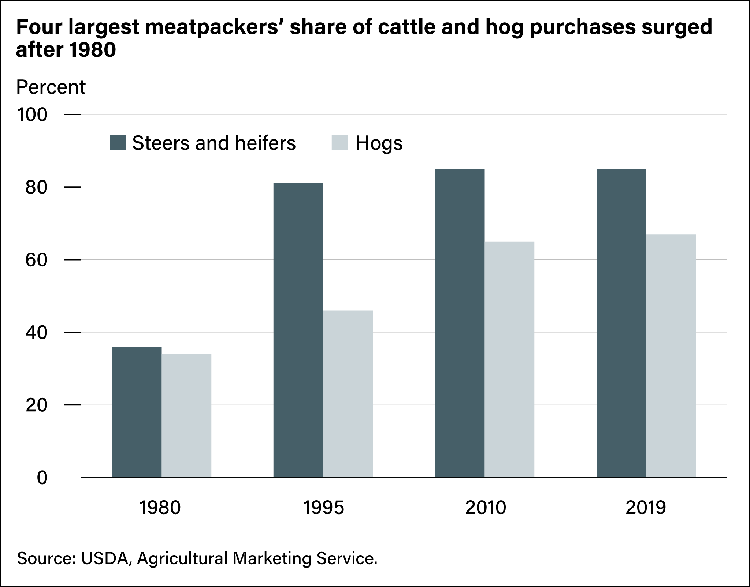

Meatpacking is a concentrated industry, with the four largest firms handling 85 percent of all steer and heifer purchases and 67 percent of all hog purchases. High concentration, and its links to competition, is a focus of recent policy initiatives aimed at encouraging more competition.

Meatpacking industries concentrated rapidly in the 1980s and 1990s. An outpouring of research followed and found only limited evidence that high packer concentration caused reduced prices for livestock.

However, in recent years there is evidence of reduced competition in meatpacking, with lower prices for cattle. This evidence is reflected in sharply increased spreads between cattle prices and wholesale beef prices, the disappearance of excess capacity in packing plants, and recent entry into the industry by new packers. Entry and capacity expansion could encourage renewed competition in the industry.

Click here to view a detailed analysis conducted by USDA’s Economic Research Service.