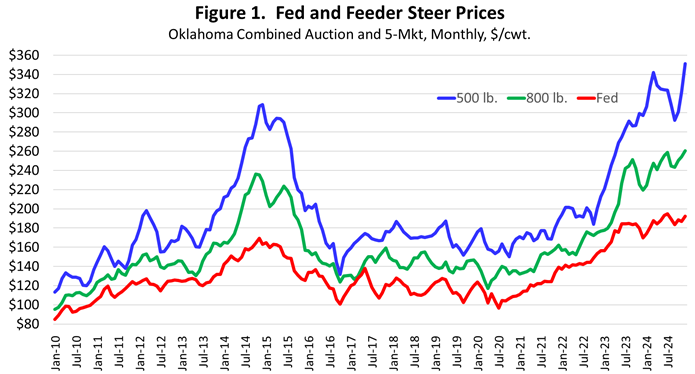

The average price this year was up 18.6 percent year over year and was up 62.6 percent over 2022 levels.

Derrell S. Peel, Oklahoma State University

Feeder auction trading is finished for the year with new record prices in 2024. Combined Oklahoma auction prices for 500-pound steers (M/L, Number 1) averaged $320.14/cwt. with the highest weekly price of $360.99/cwt in early December. The average price this year was up 18.6 percent year over year and was up 62.6 percent over 2022 levels. The 2024 average price exceeded the previous record high in 2015 by 21.3 percent.

The average price of 800-pound steers (M/L, Number 1) this year was $247.43.cwt, up 14.7 percent year over year and up 50.5 percent over 2022 levels. The highest weekly price for these big feeder steers was $264.74/cwt. in early July and only slightly below that in December. The 2024 average price exceeded the previous annual record in 2015 by 21.6 percent.

Just a few more fed cattle are expected to trade to wrap up December. The 5-Market average fed price for 50 weeks through mid-December was $186.66/cwt., up six percent year over year and up 29.2 percent over 2022 fed prices. The 2024 average price is 21.3 percent higher than the previous high price in 2014. The highest weekly fed price was $197.09/cwt. in early July and is expected to end the year with prices close to that level.

Figure 1 above shows how feeder and fed cattle prices have developed over the past 15 years. The current high prices are reminiscent of the cyclical peak prices of 2014 – 2015 with both having been provoked by drought exaggerated herd liquidations. However, some very important differences mean that the current situation will play out in a much different fashion going forward. The herd rebuild in 2014 – 2019 was sharp and rapid, leading to relatively brief high prices lasting about two years. This was possible because the pipeline of replacement heifers had been building prior to herd expansion. With two years of high prices already in 2023-2024, there is no indication that cyclically high prices will be as short lived as a decade ago. The pipeline of replacement heifers has continued to be depleted to this point. The cattle industry has shown no signs of attempting to rebuild the herd yet and the process will be slower when it does happen. The peak prices in 2014-2015 coincided with increased heifer retention that squeezed feeder supplies to the tightest levels. Since no heifer retention has occurred yet, the highest prices are ahead, possibly in 2025 but more likely beyond.

The inventory status of the cattle industry will be revealed in the annual Cattle report from USDA-NASS in late January. Many cattle producers will be receiving the annual inventory survey shortly. Producers are encouraged to complete the survey to provide good information for the industry. Reliable, accurate responses from producers is the only way for all producers, the industry and analysts to have timely and comprehensive information in order to plan and manage for the coming months and years.