Derrell S. Peel, Oklahoma State University

The November 22, 2024 announcement that New World screwworm was detected in southern Mexico resulted in the temporary suspension of live cattle imports from Mexico. This raises many questions about the implications this might have on U.S. cattle markets. Some history and context are helpful to understand the potential impacts.

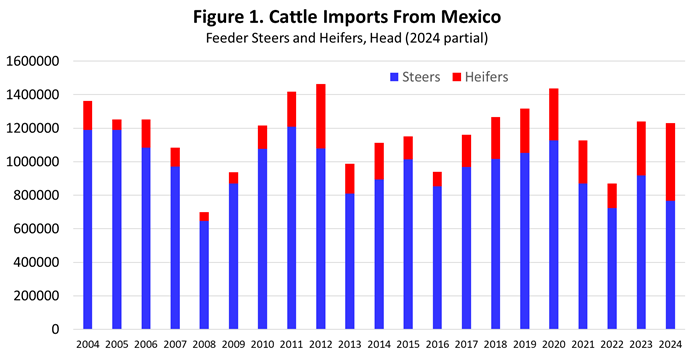

An average of 1.17 million head of Mexican cattle were imported into the U.S. in the 20 years from 2004-2023, ranging from a minimum of about 703,000 head in 2008 to a maximum of 1.47 million head in 2012 (Figure 1). Mexican cattle imports represent 3.3 percent of the total U.S. calf crop on average. Figure 1 also includes 2024 preliminary weekly imports through the first 47 weeks of the year. Imports of Mexican cattle have averaged 84.5 percent steers and 15.5 percent spayed heifers over the past 20 years (Figure 1). However, in the five years from 2019-2023, the percentage of heifers increased to an average of 21.3 percent.

Figure 2 shows the average seasonal pattern of Mexican cattle imports for the last five years. Mexican cattle imports have maintained a relatively stable seasonal pattern for many years with peak months in the spring and in November/December with lows in summer. In recent years the seasonal pattern has equalized slightly with fractionally lower peak months and higher summer lows. However, the pattern remains as seen in Figure 2.

USDA has indicated that the border is expected to be closed at least three weeks from the late November announcement. Protocols are being developed for a partial opening of the border (New Mexico and Arizona ports) which will include a pre-export inspection of all cattle; treatment for insects; and a seven-day quarantine, followed by the usual border inspection and crossing process. It seems likely that few, if any, additional Mexican cattle will be imported in 2024. The 2024 import value in Figure 1 is based on the preliminary weekly data through November 23 with a total of 1.24 million head. This may well be very close to the import total for the year.

Figure 3 shows the year-to-date monthly official import totals through September. Imports of Mexican cattle were up 21.3 percent year over year for the first nine months of the year. The pace suggested that total annual imports could be about 1.5 million head. Most of the increase was due to additional spayed heifer imports, up 87.2 percent year over year and accounting for 35 percent of total cattle imports.

Figure 2 shows that November and December typically account for roughly 22 percent of annual imports. Assuming no imports for the last week of November and all of December and given the pace of imports thus far in the year, it is likely that annual imports will be reduced by 200,000 - 250,000 head from the probable total before the screwworm announcement.

The lack of Mexican cattle imports for the remainder of the year will have some immediate impact reducing an already tight feeder supply. However, some of the feedlot impact is not immediate because a portion of the imported Mexican cattle are lightweight and typically go through stocker/backgrounding programs before feedlot placement. In the January – September period this year about 24 percent of the imported cattle were less than 200 kilograms (441 pounds). It’s important to remember that most of the cattle not imported for the remainder of the year will enter the U.S. eventually…just with a delay. As long as the current situation does not drag out excessively or result in some permanent changes in import regulations, the primary feeder cattle market impact will be a change in timing with a short-term tightening of supply and the delayed cattle arriving in the coming weeks/months.