Source: University of Michigan

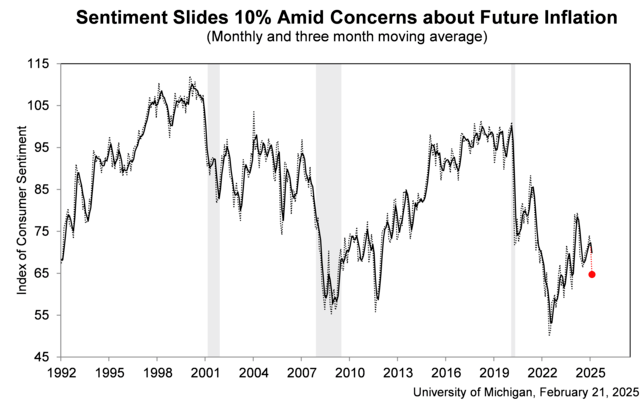

Consumer sentiment extended its early month decline, sliding nearly 10% from January. The decrease was unanimous across groups by age, income, and wealth. All five index components deteriorated this month, led by a 19% plunge in buying conditions for durables, in large part due to fears that tariff-induced price increases are imminent. Expectations for personal finances and the short-run economic outlook both declined almost 10% in February, while the long-run economic outlook fell back about 6% to its lowest reading since November 2023. While sentiment fell for both Democrats and Independents, it was unchanged for Republicans, reflecting continued disagreements on the consequences of new economic policies.

Year-ahead inflation expectations jumped up from 3.3% last month to 4.3% this month, the highest reading since November 2023 and marking two consecutive months of unusually large increases. The current reading is now well above the 2.3-3.0% range seen in the two years prior to the pandemic. Long-run inflation expectations rose over the course of the month and climbed from 3.2% in January to 3.5% in February. This is the largest month-over-month increase seen since May 2021. For both short- and long-run inflation expectations, this month’s increases were widespread and seen across income and age groups. Inflation expectations rose this month for Independents and Democrats alike; they fell slightly for Republicans.