Derrell S. Peel, Oklahoma State University

The annual Cattle report from USDA-NASS at the end of January showed that the U.S cattle industry continued to get smaller in 2024. The inventory of all cattle and calves was 86.66 million head, down 0.6 percent year over year. This total inventory was 1.8 percent lower than the recent cyclical low in 2014 and the lowest since 1951. The all cattle and calves inventory has decreased 8.0 million head (8.5 percent) from the cyclical peak in 2019.

The beef cow herd on January 1 was 27.86 million head, down 0.5 percent year over year and 3.8 percent below the previous low in 2014; the lowest since 1961. The beef cow herd has declined 3.78 million head from the recent peak in 2019, a decrease of 11.9 percent in six years. The January 1 inventory of beef replacement heifers was 4.67 million head, 1.0 percent less than one year ago and the smallest inventory since 1949. The 2025 beef replacement heifer inventory is down 9.0 percent from the previous low in 2011.

The dairy cow inventory in this report was 9.35 million head, unchanged from last year. The inventory of dairy replacement heifers was 3.9 million head, down 0.9 percent year over year. The inventory of bulls was 2.01 million head, down 0.6 percent from one year ago.

Other inventory categories are used to calculate the estimated feeder supply outside of feedlots. This includes the sum of other heifers (down 1.0 percent); steers 500+ lbs., (down 0.6 percent); and calves <500 lbs. (down 0.2 percent) adjusted for January 1 feedlot inventory (down 0.9 percent) resulting in a feeder supply estimate down 0.5 percent from last year.

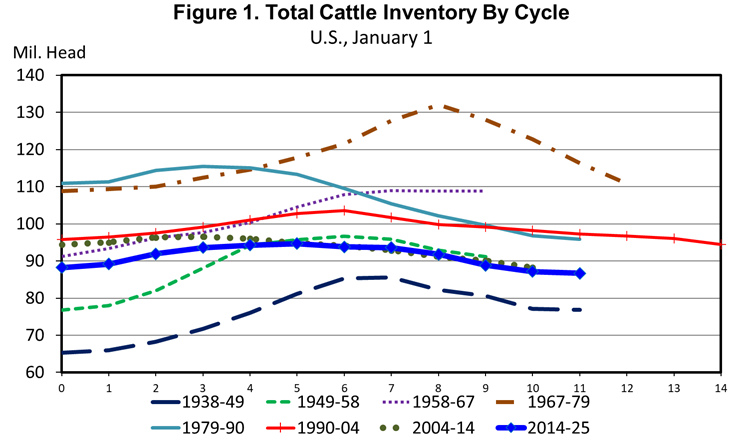

The cattle industry is characterized by so-called “10-year” cattle cycles. In fact, the last eight cattle cycles have varied from 9 to 14 years with only one (2004-2014) exactly ten years from low-to-low inventory (see Figure 1 above). The 2025 inventory represents the eleventh year since the previous cyclical low. Is 2025 the cycle low? Maybe, but not necessarily. We won’t know for sure for another year.

For 2025, the die is mostly cast relative to herd dynamics. The small inventory of beef heifers calving in 2025 (a part of the total beef replacement heifer inventory) suggests that little, if any, growth in the beef cow herd is likely. With bred heifers determined for the year, it will depend on cow culling. The cow culling rate in 2024 dropped to 10.2 percent (from higher levels in 2021-2023), about equal to the previous twenty-year average. Another year of sharp decrease in beef cow culling could lead to minimal herd growth but, lacking that, the cow herd could shrink a bit more this year. In the last three herd expansions, the cow culling rate has averaged below nine percent. In 2025, beef cow slaughter will have to drop more than 12 percent year over year to result in a cow culling rate below 9.0 percent.

The question of heifer retention in 2025 will determine herd dynamics in 2026 and beyond. Heifers saved for breeding (part of the 2025 beef replacement heifer inventory) and additional unplanned (or impulse) heifer breeding in 2025 may result in a modest increase in heifers calving in 2026. The supply of heifers available to do this is limited but could allow for limited herd growth in 2026. Additional retention of heifer calves in 2025 (for breeding in 2026) might set the stage for more rapid herd growth in 2027 and beyond. We shall see.