The biggest threat to cattle and beef markets is the potential loss of consumer demand that would result from a significant macroeconomic meltdown.

Derrell S. Peel, Oklahoma State University

Cattle prices continue to generally grind higher amid a whirlwind of political activities and rhetoric that have buffeted markets at all levels. Markets have been whipsawed with on-again, off-again political announcements that create debilitating uncertainty in equity, futures and cash markets with negative impacts on producers, consumers and the complex supply chains of agricultural and food markets.

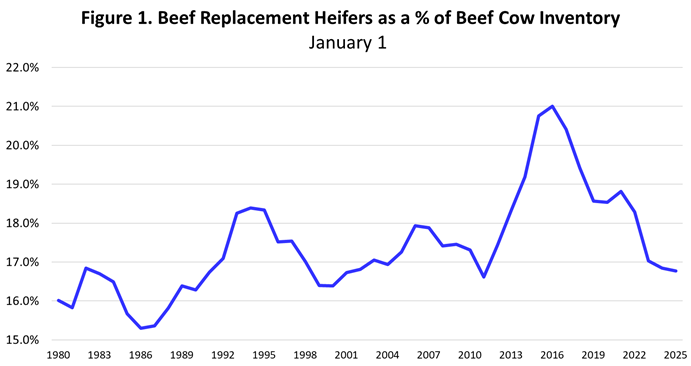

Despite that, ever tightening supply fundamentals are supporting higher cattle and beef prices. Feeder cattle of all classes and fed cattle have set new record high prices since the beginning of the year. Estimated feeder supplies outside of feedlots on January 1 were down 0.5 percent year over year. The number of heifers in feedlots on January 1 was down 3.4 percent year over year with heifers making up 38.7 percent of total cattle on feed. The January 1 inventory of beef replacement heifers was down 1.0 percent year over year and beef replacement heifers as a percent of the beef cow herd is at the lowest level since 2011 (See Figure 1 above). All of these indicate that no heifer retention was underway at the end of 2024.

Heifer retention could begin and may be starting at this time. While there is no data to verify yet, every year some level of unplanned (impulse) breeding of heifers (not designated as replacements) occurs and this typically accelerates in the early stages of herd expansion. These heifers are currently included in the “Other Heifer” category of inventory and are part of the estimated feeder supply. If impulse heifer breeding increases this year, it will represent a one-for-one reduction in feeder supplies and will increase bred heifers entering the herd in 2026. Additionally, heifer calves may be retained in 2025 for breeding in 2026 and calving in 2027. All of this will lead to reduced feeder supplies though 2025 and beyond, further supporting feeder cattle prices. Even if cattle producers are ready and intend to begin herd rebuilding, drought threats remain that may limit what is possible.

Consumers can expect to continue seeing high beef prices that may push even higher in the coming months. Heavier carcass weights helped maintain beef production in 2024 and will continue to do so this year. Eventually, however, reduced cattle slaughter will reduce beef production. Beef markets will ration smaller beef supplies with even higher beef prices as long as demand remains robust.

Uncertainty and volatility from external turbulence will likely continue to impact cattle markets. However, as long as these do not result in a major macroeconomic disruption (i.e. recession), cattle markets are expected to continue strong. The biggest threat to cattle and beef markets is the potential loss of consumer demand that would result from a significant macroeconomic meltdown. Fasten your seatbelts, cattle markets are gaining altitude, but turbulence is expected.

Articles on The Cattle Range are published because of interesting content but don't necessarily reflect the views of The Cattle Range.